During the third quarter of 2016, the Seafarer Overseas Growth and Income Fund gained 4.61%.1 The Fund’s benchmark, the MSCI Emerging Markets Total Return Index, rose 9.15%. By way of broader comparison, the S&P 500 Index gained 3.85%.

The Fund began the quarter with a net asset value of $11.50 per share. The Fund paid no distributions during the period, and finished the quarter with a value of $12.03 per share.2

Performance

During the third quarter, the benchmark rose sharply, led by gains in Chinese internet companies and financial service firms. While China contributed the most to the index’s increase during the quarter, most other developing countries saw their equity markets advance. The broad-based gains ostensibly were prompted by two events: the reduced likelihood of an interest rate increase in the U.S., and renewed optimism regarding the health of the Chinese economy.

At the outset of the third quarter, global investors expected that the U.S. Federal Reserve (the “Fed”) would enact at least one rate increase well before the end of the year, and possibly more. However, data released during the quarter suggested that, while the U.S. economy was firm, it was not so strong as to necessitate a near-term rate hike. Speculation rapidly veered in the opposite direction, such that many forecasts suggested that the Fed would not act until very near the end of the year, and possibly not until 2017.

The resulting shift in forecasts spurred gains in many asset classes. Emerging market currencies, equities and bonds were particular beneficiaries of the changing sentiment. Importantly, most emerging market currencies were relatively stable versus the U.S. dollar, in contrast with the preceding four years, during which the U.S. dollar’s strength consigned the emerging market asset class to prolonged weakness. The recent stability among currencies might not persist, but in the shortest run it has been essential to underpinning broad-based enthusiasm for stocks and bonds from the developing world.

Within the developing world, Chinese shares led the way: the MSCI China Index rose 13.97% during the quarter. China’s performance was a reversal of the first half of the year, during which global investors sold off Chinese shares, presumably based on perceptions that the economy was struggling and that the local currency (the renminbi) was ripe for a sharp fall. (For the record: the currency declined by 4.3% versus the dollar as of the date of this report – far less than some of the dire predictions made at the outset of the year.3) Data on the Chinese economy published during the third quarter was mixed; some indicators suggested a moderate improvement, and others implied weakness. Ironically, the resulting ambiguity spurred gains in equities: some investors speculated that the muddled data would provide an excuse to the Chinese government to embark on another round of credit-driven stimulus. The shares of Chinese banks and insurance companies rose steadily in response.

Strength in Chinese shares, stable currencies, and the receding likelihood of a U.S. rate hike all combined to spur broad-based enthusiasm for emerging market assets. Nearly every constituent country within the MSCI Emerging Market Index – and every constituent sector – contributed to the benchmark’s increase during the quarter.

Amid the swift and broad-based rally, the Fund’s absolute performance was strong, but it fell short of the benchmark’s gains. There are at least three ways to understand the Fund’s shortfall. First, it can be explained in terms of relative positioning: the Fund’s underweighting to Chinese shares, particularly financial institutions and internet companies, created much of the performance gap. Second, it can be explained in strategic terms: historically, Seafarer’s growth and income strategy has tended to lag the overall market during short-term periods of sharp gains. Third, and perhaps most importantly, it can be explained in macro-economic terms: contrary to the preceding five years, investors’ expectations for earnings growth in the developing world is no longer grossly misaligned with reality – and reality has improved a bit. As the “expectations gap” has narrowed, investors have rotated their portfolios to favor cyclical companies that might enjoy a rapid recovery in profit growth. The underlying premise is that the earnings cycle in the emerging markets has turned for the better. In contrast, the Fund invests in companies that Seafarer believes are capable of sustainable growth – and this means that when the market anticipates a cyclical recovery, the Fund is inevitably positioned poorly to capture the full benefit of the recovery.

I will briefly elaborate on these three points. Regarding the first point: I will discuss the Fund’s underweighting to China and internet stocks in the Allocation section of this review, below.

Regarding the second point: the Fund has two objectives, namely long-term capital growth, with some income, and the mitigation of adverse volatility. The Fund follows a growth and income strategy in order to achieve these two objectives. Typically the strategy favors companies that Seafarer believes are capable of growing slowly, but steadily.

In addition, I favor companies that I believe can produce sufficient cash flow to sustain a steady dividend even during extended periods of weak economic growth. This means that the Fund often holds shares that have valuations that are moderately in excess of the market average, particularly when measured in terms of price to earnings multiples. The market often awards slightly higher valuations to these steadily-performing companies, particularly during periods of anemic performance overall.

The problem is that, when earnings have the potential to accelerate dramatically – particularly during a perceived cyclical “bottom” in earnings – the strategy has historically lagged the market, sometimes substantially. The steadiness I seek typically does not capture the full benefit of recovery, which tends to favor nominally cheaper, cyclically-depressed shares. In other words: the market tends to rotate its attention to companies that might experience a dramatic restoration of profitability (and consequently, the share price might exhibit a substantial gain). I do not offer this explanation as an excuse, but rather as context for what to expect from the Fund’s investment strategy over time.

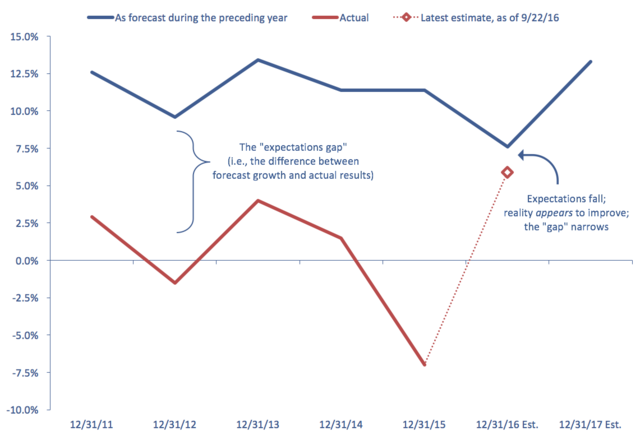

This leads to the third point: growth in earnings might be recovering, after many years of anemic conditions. The chart below shows two lines. The blue line represents forecast growth in corporate profits, based on consensus estimates. The red line represents the growth that was produced in reality. As you can immediately see, the period between 2011 and 2015 was subject to an immense “gap” in expectations: the forecast for growth was high, even as reality was chronically disappointing.

- Past performance does not guarantee future results.

- Source: J.P. Morgan, "Emerging Markets Strategy Dashboards," 2011-2016.

Yet, the data suggests that this situation may be changing. Forecasts for 2016 were lower (and consequently more realistic). At the outset of the year, consensus expectations suggested roughly 8% annual growth in profits. As of September, the latest measurement points to 6% growth this year – still below target, but the “gap” is by no means as large as it has been in the past.

Personally, I believe two conditions have dominated investment in the emerging markets over the past five years: first, the weakness of emerging market currencies (or, conversely the pronounced strength of the U.S. dollar); and second, the widening – and more recently, the narrowing – of the “expectations gap.” I think the latter condition explains in simple terms much of what anyone needs to know about why the emerging markets have been weak prior to 2016: expectations for growth were high; investors bid up shares in anticipation; and the reality was anemic for five consecutive years. Now, the reverse might be true, at least in 2016: expectations were more reasonable; valuations were considerably lower; and it appears that reality might meet the subdued expectations. Frankly, other than the dollar’s waxing and waning, this is in my opinion the essential narrative that explains why emerging markets have behaved as they have over the past five years.

This condition also explains why the Fund has met with success in the past, and why the Fund may not do so (or may not do so to the same extent) in the future. The Fund’s strategy seeks to invest in the securities of companies that Seafarer believes offer the prospect of steady income and sustainable growth. During a period characterized by anemic growth, such securities tend to stand out against the market. Under different conditions – particularly conditions where growth might be recovering, and some companies might produce results in the short run that surpass low expectations – the Fund’s discipline might act as a short-term impediment to its success.

Shareholders should take note: if earnings growth is set to recover, the Fund might well lag the market’s reaction, especially if the market moves swiftly higher. However, it is not a foregone conclusion that a recovery is underway; I will return to that question in the Outlook section below.

Allocation

During the course of the quarter, the Fund added one new holding, the common stock of Coway Company, Limited.

Coway is based in South Korea, and is a relatively unique business: it leases high quality consumer products to individual households, on a “lease-to-own” basis. The company is known particularly for its air and water filters, but it also leases (or sells) a number of other products, including bidets, mattresses and kitchen appliances. The company’s products are meant to promote healthy living and sanitary conditions in urban centers – pure water, pure air, hyper-clean mattresses, etc. The company operates primarily in Korea, but it also has a burgeoning business in Malaysia, and is attempting to expand into both the U.S. and China.

Perhaps what makes the company most unique is that, within Korea, its products are leased and serviced by a network of trained, door-to-door sales agents known as “CODYs.” The name is a bit awkward, but it is meant to merge the terms “Coway” and “lady.” The CODYs are well-trained and very professional in their service of customers; they make door-to-door house calls, assessing whether each customer is satisfied with the product, and inquiring as to whether the customer needs to purchase a replacement filter or a mattress cleaning service.

There are a host of aspects that make the business attractive in my view. Currently, a Korea-based private equity group controls the company. That private equity firm helped hive Coway off from a Korea-based conglomerate that had saddled the company with too much debt (Coway was the conglomerate’s “cash cow”). The private equity group has done an above-average job turning the company around, namely by reducing debt, reducing customer defections, reducing costs, and enhancing the CODY network to stabilize sales. I think these efforts have left the company in a good position for the future. Coway’s leasing arrangements ensure relatively predictable cash flows, and the high-touch sales model helps generate slow but steady growth. Coway’s success hinges on whether it can develop new product categories, successfully enter new geographies, and fend off rising competition. If it does so, I think it can accelerate its earnings growth and dividends such that the yield could rise roughly 25% to 30% over the next three years, making it an attractive holding for the Fund.

In the Performance section above, I wrote that I would discuss the Fund’s underweight positions in China, especially in Chinese internet stocks.

Regarding China: above all, I remain steadfastly of the view that China is the most important country within the emerging markets. The country’s economic emergence has defined the asset class over the past two decades, and I believe its continued evolution over the next two decades will again dictate terms for the asset class. China’s long-run emergence is essential to the investment merits of the developing world. If you harbor serious doubts about whether China is a viable long-term investment destination (i.e. you believe it will eventually be revealed as a failed nation-state and economy, permanently), then I would suggest you exit the asset class, and do not look back.

Yet despite my high degree of conviction in China’s long-run evolution, I am concerned about its near-term status. The risk of a financial crisis, induced by poor liquidity conditions and weakened solvency, are elevated compared to the country’s history. It is by no means a foregone conclusion that a severe event will occur. I believe the odds are still low, and should not figure in anyone’s basic assumptions about the future. Yet the risk cannot be ignored, and in fact should be given more credence than was the case in the past two decades (when alarm was also raised many, many times – but on very weak grounds, in my opinion).

I am a “bottom-up” investor, which means that when I select securities for the Fund, I do so based on my assessment of their individual merits – and not based on a sweeping view of the macro-economic landscape. Thus I do not make blanket judgments to avoid China, even as I believe risks there are elevated. However, when I examine the financial strength and outlook of individual companies in China, I do believe the picture is murkier now than it was in the past. As such, it is currently harder to find individual companies in China capable of producing the sort of sustained growth and yields that the Fund seeks – even as I do not arrive at that conclusion “from the top down.”

Within China, the internet sector has given me the most trouble. There are a number of internet firms that have produced incredible growth and substantial free cash flow; some even now pay meager dividends (most do not). Since its inception, I have steered the Fund such that it passed over this sector entirely. In hindsight, my decision was a poor one: large capitalization Chinese internet stocks have proven to be one of the best-performing sub-sectors over the past five years. The companies in the sector have grown mightily and prospered, and their stocks have followed suit.

The trouble I have had with these stocks is that they have never come close to fitting within the parameters that I seek for the Fund’s growth and income strategy. In my own words, the Fund’s strategy attempts to find high quality companies capable of producing sustained growth in free cash flow. I use the current income that the company produces (usually manifest in dividends, but sometimes in bond coupons) as a key means to assess the attractiveness of the growth. First, we use the income to value the growth; we do not want to overpay for the growth, and the yield helps us measure a given security’s valuation. Second, we attempt to use the income as a means to dampen volatility in the portfolio. Third, we use the income as means to vet the underlying liquidity and solvency of the company’s business model. We believe that when a company can regularly pay out a substantial portion of its earnings, it is demonstrably more liquid (and therefore, probably more solvent) than a company that cannot or will not do so.

This is the rub with the Chinese internet stocks: they have always enjoyed very elevated valuations, but have paid scant dividends, and then only recently. While in hindsight their elevated valuations appear warranted, they have never generated enough current income to satisfy the conditions that I use to assess most prospective investments. It is a sector that haunts me, a bit: on one hand, I am proud that the Fund has outperformed historically, without the benefit of investment in one of the best-performing and widely-held sectors. At the same time, some of the companies in the sector are a bit like Moby Dick for me: they are the big ones, and they have gotten away.

Outlook

Returning to the question of whether the emerging markets are experiencing a recovery in earnings growth: in my view, the evidence is tentative at best. Yes, the “expectations gap” appears to have narrowed based on a measure of aggregate corporate earnings. I think investors should recognize there is a fundamental basis for the recent performance in emerging market equities: stocks have not risen reflexively simply because they were “too cheap” relative to the rest of the world, but rather because the gap between expectation and reality has closed. Furthermore, investors should remain open to the idea that profit growth in the emerging markets might be recovering.

At the same time, I would stress that the growth I can observe is tepid, and the conditions that have closed the “gap” are tenuous. Personally, when I examine the results of companies within the Fund’s portfolio, or even a broader set of companies that I follow, I do not see evidence that a strong recovery is underway. In fact, I would suggest the recovery is feeble, and may disappoint yet again. The margin of disappointment may be less extreme than was the case during the past five years. Still, I would not be surprised if the final results fall below the 6% growth estimate for 2016, as depicted by the dashed red line in the “expectations gap” chart above.

Given the precarious circumstances – growth has improved, but not as much as the market’s ebullient performance would suggest – I recommend that investors tread cautiously, and treat the recent rally as a speculative one. In general, stock markets tend to speculate on the possibility of recovery well before there is evidence of improvement. As such, it is quite possible that the market has “run ahead” of the fundamentals, and there could be scope for disappointment in the coming quarters. In summary: investors should stay open to the possibility of fundamental recovery, but avoid extrapolating the trend too far, too fast.

We appreciate your decision to entrust us with your capital. We are honored to serve as your investment adviser in the emerging markets.

Andrew Foster,- The performance data quoted represents past performance and does not guarantee future results. Future returns may be lower or higher. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. View the Fund’s most recent month-end performance.

- The MSCI Emerging Markets Total Return Index, Standard (Large+Mid Cap) Core, Gross (dividends reinvested), USD is a free float-adjusted market capitalization index designed to measure equity market performance of emerging markets. Index code: GDUEEGF. It is not possible to invest directly in this or any index.

- The MSCI China Index is a free float-adjusted equity index that tracks large and mid-capitalization companies across China H-shares, B-shares, Red chips and P chips. The Index does not include China A-shares. The Index represents common stock in Chinese companies that is available for investment by foreign (non-mainland China) investors. Index code: GDUETCF. It is not possible to invest directly in this or any index.

- The S&P 500 Total Return Index is a stock market index based on the market capitalizations of 500 large companies with common stock listed on the NYSE or NASDAQ. It is not possible to invest directly in this or any index.

- The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer's current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Seafarer does not accept any liability for losses either direct or consequential caused by the use of this information.

- As of September 30, 2016, Coway Co., Ltd. comprised 3.3% of the Seafarer Overseas Growth and Income Fund. View the Fund’s Top 10 Holdings. Holdings are subject to change.

- References to the “Fund” pertain to the Fund’s Institutional share class (ticker: SIGIX). The Investor share class (ticker: SFGIX) gained 4.62% during the quarter.

- The Fund’s Investor share class began the quarter with a net asset value of $11.47 per share; it finished the quarter with a value of $12.00 per share.

- Bloomberg, 25 October 2016.

![[Chrome]](/_layout/images/ua/chrome.png)

![[Firefox]](/_layout/images/ua/firefox.png)

![[Opera]](/_layout/images/ua/opera.png)

![[Microsoft Edge]](/_layout/images/ua/edge.png)